Multifamily Syndications

Multifamily Demand Backstory

The U.S. housing market has been out of balance for years. Home prices have outrun wage growth, construction costs keep rising, and starter homes that once took one income now take two. More households are being pushed into renting, not by preference but by math.

At the same time, new supply hasn’t kept pace. Developers are dealing with zoning delays, labor shortages, and higher financing costs. Fewer new projects get built each year, widening the gap between what families need and what exists.

Here’s the part most people miss:

According to CBRE, renters absorbed over 300,000 apartment units last year, in a year with higher rates and a cooling economy.

That’s roughly 3× more demand than we normally see in a slow market. In other words, even when the headlines looked shaky, renters kept filling apartments.

Strong demand meets a different problem: most of the apartment stock in the U.S. is aging faster than we can replace it.

New construction is expensive, slow, and heavily regulated. In many cities, you simply can’t build enough new supply to meet demand, zoning, permitting, and financing won’t allow it.

That creates a strange kind of pressure: renters need quality housing, but operators can’t build their way out of the shortage. So the opportunity shifts to the existing stock.

This is why value-add exists.

Instead of building new, operators buy older properties and upgrade them, improving the units, tightening operations, and bringing the property up to the standard today’s renters are willing to pay for.

When you see the demand picture and the supply constraints together, the value-add model stops feeling like a “strategy” and starts looking like market physics.

When market structure, credit conditions, or capital flows shift, I send a short analysis of what it means for risk, liquidity, and cash flow resilience.

Only when something actually changes.

Get the next Back9 Signal →

Multifamily Value-Add Playbook

Now that the demand drivers are clearer, the next question becomes:

What exactly are operators doing inside these deals to create returns?

That’s where the model comes into focus.

If you have ever read a multifamily investment summary and thought, “This feels more complicated than it needs to,” you are not alone. Many investors see the headline returns without understanding the mechanism underneath.

The truth is simple. A value-add multifamily syndication is essentially flipping an apartment complex over three to five years, with tenants in place and a professional team running the playbook.

Think of it like upgrading an enterprise application without taking production offline—running a phased migration while the system stays live, or rebuilding the engine while the car stays on the road.

The Six-Phase Workflow

No hidden steps. No guesswork. When you see the phases laid out like this, the pieces you hear about, including value-add, refinancing, and distributions, tend to fall into place.

You are not flipping countertops. You are flipping the income stream.

How Value Is Actually Created

1. NOI- the income engine

NOI just means “the property’s income after expenses.”

When that number goes up, the property becomes more valuable. Not because of emotion, hype, or comps… but because apartments are valued like businesses.

Think of it like upgrading software from the free tier to the enterprise license, the pricing power changes instantly.

You renovate units so you can charge $75 more per month. Watch what happens to the property value:

NOI Example: Small Rent Increase → Big Value Jump

That’s why great operators obsess over the NOI engine, small changes compound big.

$75 × 12 months = $900 more income per unit per year.

Multiply that across 100 units → $90,000 more annual income.

That extra income plugs straight into NOI.

And in many markets, every additional $1 of NOI adds $15–$20 in property value.

So a modest $90K bump in annual income could add $1.3–$1.8 million in value.

2. Forced Appreciation: The value you create, not wait for

Forced appreciation isn’t waiting for the market to cooperate.

It’s the result of deliberate operator pressure applied to income, expenses, and operations and letting the math do the rest

In single-family homes, you wait for the market to lift your value.

In apartments, you manufacture the value.

Forced appreciation comes from:

Improving the property (renovations, amenities, curb appeal)

Improving operations (better management, tighter expenses, smarter pricing)

It’s called forced because you’re not waiting for the market —

you’re making changes that mathematically raise income and reduce waste.

- Older interiors and limited amenities.

- Looser operations, higher day-to-day expenses.

- Rents stuck at “good enough” for the neighborhood.

- NOI is lower than it could be, so property value is capped.

- Renovated units and better amenities support higher rents.

- Tighter operations reduce waste and control expenses.

- NOI increases because revenue is up and leaks are plugged.

- Higher NOI is capitalized into a higher property value.

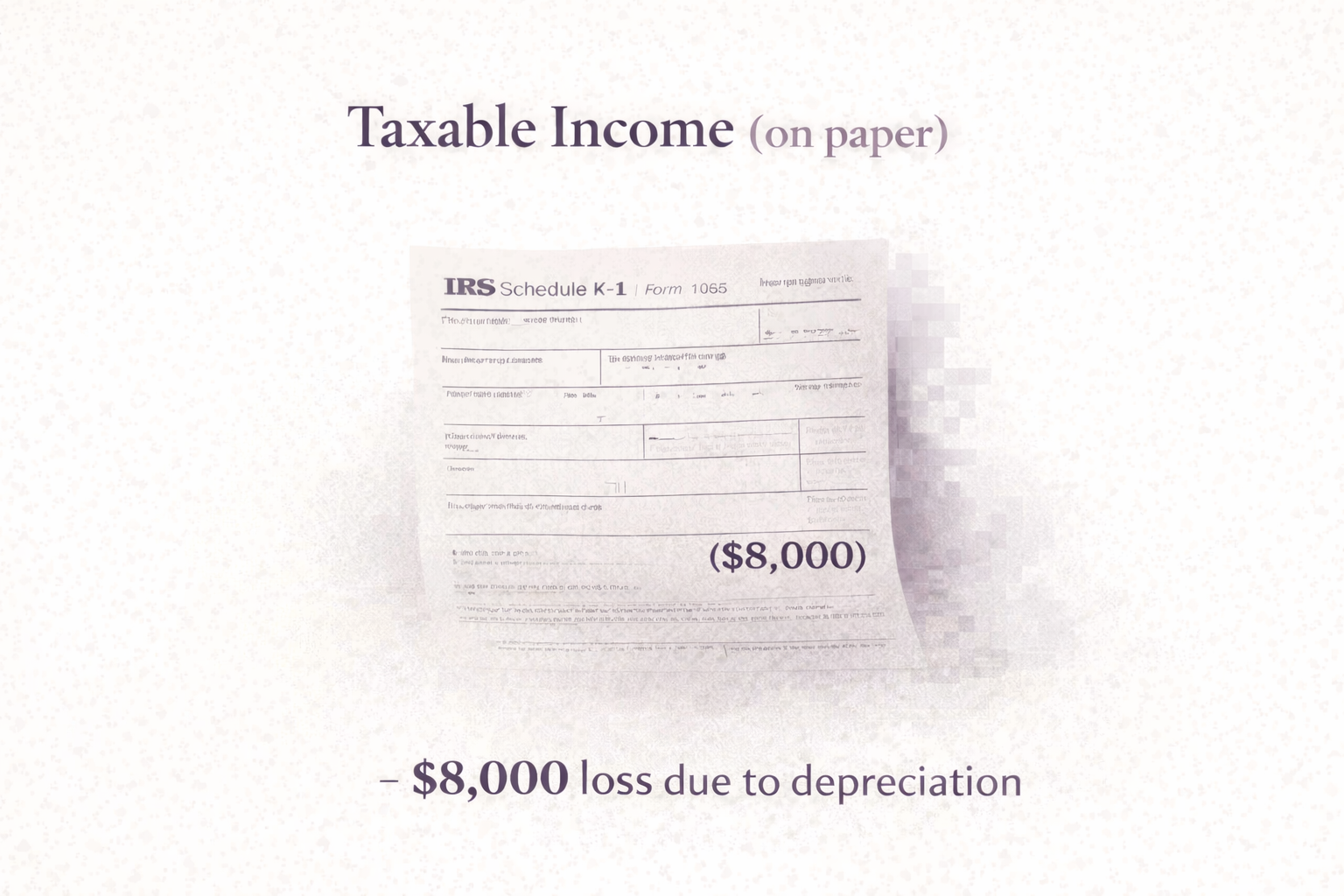

3. Depreciation: A tax benefit that shelters your cash flow

IRS depreciation rules (IRC §167 & §168 These IRS code sections allow real estate owners to deduct the “wear and tear” of a building over time — creating a paper loss that can offset cash flow. In multifamily deals, investors receive their proportional share of this deduction through the LLC structure. ) act like a firewall around your cash flow.

Because apartment deals are normally owned through an LLC, investors get a proportional share of depreciation, a paper loss created by the IRS to account for the building aging over time.

But here’s the trick:

The property might be cash-flowing beautifully…

while the depreciation shows a loss on paper.

Example:

- You invest $100K.

- You receive ~$6K in distributions that year.

- You might get $8–$10K in depreciation allocation.

- On paper, that shows up as a tax loss.

→ a tax loss (you owe zero taxes).

That’s why people love multifamily. Depreciation acts like a firewall around your cash flow, especially when operators use cost segregation Cost segregation is an IRS-approved method (under MACRS rules) that accelerates depreciation by reclassifying parts of a building into shorter-life asset categories — producing larger paper losses earlier in the hold period. to accelerate it.

How I Think About This Today

By now, you should have a clear picture of how multifamily syndications actually work, not as speculation, but as a repeatable operating model.

Income drives value.

Improvements compound.

And the tax benefits protect your cash flow while the deal works quietly in the background.

I’ve invested in and partnered on over 50 multifamily transactions across multiple cycles, including strong runs and uncomfortable lessons.

If it’s helpful, I’m happy to walk through how I think about this model today, what I look for in operators, and where I’ve adjusted my lens.

If you want the full framework, the

Inside

L00K

walks through the model step by step.

If you’d rather talk it through, you can book a short call instead.

This article is for educational purposes only and does not constitute investment advice or an offer to sell securities.