Inside L00K: The Hidden Value-Add Inside Dental Practices

The Hidden Value-Add Inside Dental Practices

Why improving practice economics is often less about adding patients and more about fixing the systems that turn care into cash flow.

Utilization

1 in 3

Dentists said they were not busy enough.

Collections

98%+

Net collections target discussed by operators.

Reactivation

3,100+

Unscheduled patients in one practice example.

According to the ADA Health Policy Institute’s Q4 2025 State of the U.S. Dental Economy report, dentists’ top expected challenges for 2026 were insurance issues, staffing, and overhead costs. One-third of dentists also said they were not busy enough, up from one-quarter a year earlier.

I recently attended Henry Schein’s annual dental conference, and one theme kept showing up. Many dental practices are not failing because they lack demand. A practice can be clinically busy and still underperform financially if the systems around collections, scheduling, treatment follow-up, and reporting are not disciplined enough.

The examples were specific. Some practices were falling short of 98%+ net collections targets. Others showed meaningful revenue leakage. One case had more than 3,100 unscheduled patients, representing roughly $328,000 of immediate opportunity and $2.2 million of annual opportunity.

That is the value-add thesis in dental: buy or partner with under-managed practices, then improve the systems that turn patient care into durable cash flow.

Dental value-add works like real estate value-add, but the upgrades are harder to see.

Most investors understand value-add real estate. You buy an under-managed apartment building, renovate units, reduce vacancy, improve collections, professionalize management, grow NOI, and hopefully sell a better-performing asset at a higher valuation.

Dental practices can work in a similar way, but the “renovations” are less visible. Instead of countertops, flooring, and leasing systems, the upgrades are revenue cycle management, documentation quality, coding consistency, A/R discipline, hygiene reappointment, treatment follow-up, labor workflow, and management dashboards.

Real Estate

Renovate units. Reduce vacancy. Improve collections. Professionalize management. Grow NOI.

Dental Practices

Clean up claims. Improve collections. Reactivate patients. Tighten scheduling. Build better dashboards.

Unlike a value-add real estate project, the improvements are often invisible to patients. They show up in cleaner claims, better collections, stronger hygiene retention, improved scheduling, and more disciplined management systems.

In other words, the value-add is often not simply “more patients.” It is building a better operating system around the patient care already happening inside the practice.

That distinction matters.

A dental practice can be clinically busy and still leak revenue. It can produce a lot of dentistry and still fail to collect what it earned. It can have loyal patients and still leave meaningful treatment unscheduled. It can have good doctors and still operate with weak reporting, inconsistent billing processes, or poor visibility into future revenue.

The goal of sophisticated dental management is not to push clinicians to “do more.” It is to help the business capture more of the value it is already creating.

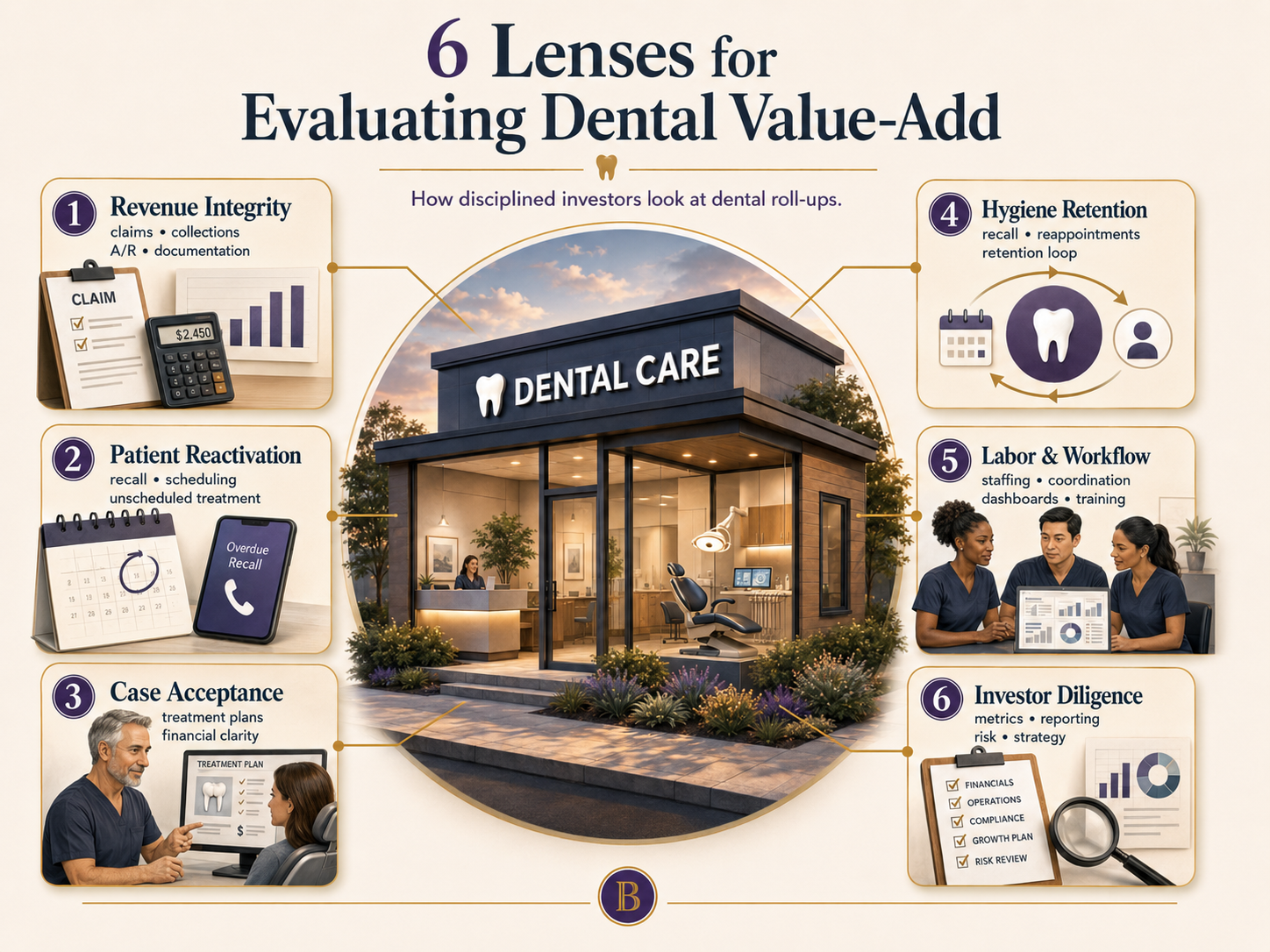

1. Revenue integrity: the first hidden lever

The most overlooked value-add category in dental is what I would call revenue integrity.

That includes claims submission, insurance verification, documentation, coding accuracy, collections, A/R management, fee schedules, payer follow-up, and appropriate medical-dental billing when the treatment is medically necessary.

This is not about “insurance tricks.” That is the wrong frame, and frankly, a dangerous one. The real issue is whether the practice is accurately documenting, coding, submitting, and collecting for legitimate care.

Revenue integrity flow

Care only becomes cash flow when the chain holds together.

Production → Documentation → Coding → Claims submission → Collections → Cash flow

A simple benchmark: well-run practices often target 98%+ net collections. Yet conference materials I reviewed cited examples of practices collecting closer to 91%, with meaningful annual leakage as a result.

That gap matters.

In real estate, rent billed is not the same as rent collected. In dental, production is not the same as cash flow.

A/R tells the story. Healthy A/R is not just “low.” It has a shape. Most of it should sit in the 0 to 30 day bucket, with very little over 90 days. One operating framework flagged A/R above 20% of monthly production as a brewing collections problem.

That is the kind of detail investors should care about. A/R is not just an accounting report. It is an early warning system.

The same applies to documentation. One example that came up repeatedly in the dental billing discussions was D2950 buildups. A well-managed practice does not simply submit the code and hope it clears. The documentation needs to support the clinical condition. That may include remaining tooth structure and photos when X-rays do not clearly show the issue.

That may sound like a small administrative detail. It is not. In an environment where claims are increasingly reviewed by automated systems and AI-assisted adjudication, the image, narrative, code, and clinical condition all need to tell the same story.

Small gaps become large numbers at scale.

2. Patient reactivation: demand already inside the building

The next value-add lever is scheduling and patient reactivation.

Many people assume dental growth requires buying more leads or adding more new patients. Sometimes it does. But often, the first opportunity is already sitting inside the practice management system.

Unscheduled treatment. Overdue hygiene. Patients who started but never completed treatment. People who said “not now” and were never followed up with properly.

Operator lens

The best operators do not just ask how to find more patients. They ask where existing demand is getting stuck.

They look for overdue hygiene, diagnosed but unscheduled treatment, patients who fell out of recall, accepted treatment plans that were never completed, and schedule holes 30, 60, or 90 days from now.

One conference example referenced more than 3,100 unscheduled patients, representing hundreds of thousands of dollars of immediate opportunity and millions in potential annual opportunity.

That is not theoretical demand. That is demand already inside the building.

In multifamily terms, this is vacancy. An empty unit produces no rent. In dental, an empty hygiene column or an ignored unscheduled treatment list produces no revenue.

That is not glamorous work. But operational value-add rarely is.

- Is dental value-add real operational improvement, or mostly multiple arbitrage?

- If these improvements are obvious, why haven't dentists already fixed them?

- How do investors know EBITDA growth isn't coming from aggressive billing or treatment pressure?

- What is the strongest bear case against dental roll-ups?

- What evidence proves the playbook can scale across dozens of practices?

- What are the biggest reasons dental roll-ups fail?

3. Case acceptance: converting diagnosis into completed care

Another major lever is case acceptance.

This is where investors need to be careful. Case acceptance should not mean pressuring patients into unnecessary treatment. It means improving communication, affordability, trust, and follow-through so clinically appropriate care actually gets completed.

A practice can diagnose appropriate treatment all day long, but if patients do not understand it, cannot afford it, or never receive proper follow-up, the revenue never materializes.

Case acceptance is not a pressure tactic. It is a coordination metric.

Case acceptance reflects the quality of the doctor’s explanation, the treatment coordinator’s process, the front desk’s financial communication, and the practice’s ability to reduce friction.

One of the more interesting conference takeaways was that being in-network can sometimes improve treatment acceptance, not just patient volume, because patients perceive treatment as more financially accessible.

For investors, case acceptance is a forward-looking revenue indicator. If case acceptance falls today, revenue may soften 30 to 60 days from now.

When market structure, credit conditions, or capital flows shift, I send a short analysis of what it means for risk, liquidity, and cash flow resilience.

Only when something actually changes.

Get the next Back9 Signal →

4. Hygiene: recurring revenue hiding in plain sight

Hygiene is often underappreciated by investors who are new to dental.

It is not just “cleanings.”

Hygiene is patient retention, recurring revenue, diagnosis flow, relationship maintenance, and future restorative production. It is one of the clearest signals of whether the practice has a durable patient base or is constantly trying to refill a leaky bucket.

A well-managed practice treats hygiene like recurring revenue infrastructure. It tracks reappointment rates. It pre-blocks recall. It follows up with overdue patients. It understands that a missed hygiene visit is not just one lost appointment. It may be the beginning of patient attrition.

Hygiene operating loop

Reappoint

Recall

Follow up

Retain

The point is not one appointment. The point is whether the practice has a system for keeping the patient relationship active.

Hygiene holes are the dental version of vacancy.

5. Labor, workflow, and management discipline

Finally, dental value-add depends on management systems.

At one location, a talented owner-doctor can often keep everything moving through sheer force of personality. By the third location, founder heroics start breaking down. Systems become mandatory.

This is where strong dental management separates itself.

The best teams manage weekly leading indicators, not just month-end financials. They track A/R, provider productivity, hygiene reappointment, case acceptance, labor as a percentage of collections, same-store growth, no-shows, denials, and schedule utilization.

They also redesign workflows.

Operating leverage

A 1% labor improvement on a $20 million dental group can equal roughly $200,000 of EBITDA.

That is why small operating gains matter. In a scaled practice group, workflow discipline does not just clean up the calendar. It can change the economics of the business.

One conference example questioned why a $22 to $28 per hour front-office employee should spend large amounts of time sitting on insurance verification calls if automation, AI tools, or outsourced workflows can handle portions of that work more efficiently.

That is not about cutting staff blindly. It is about matching task complexity to labor cost.

That is why marginal gains matter in dental. Better claims. Cleaner schedules. Fewer denials. Stronger recall. Faster collections. Less labor waste. More consistent dashboards.

None of these sound dramatic by themselves. Together, they can change the economics of a practice.

6. What investors should watch

Investors do not need to become dental billing experts. But they should understand enough to know whether an operator is actually improving the business after acquisition.

The first question is whether the practice is collecting what it produces. Production looks good on paper, but collections determine cash flow. If A/R is aging past 90 days, or if too much revenue is stuck in insurance follow-up, the practice may have more operating leakage than the headline numbers suggest.

The next question is whether the schedule is being actively managed. A strong operator should know how many patients are overdue for hygiene, how much diagnosed treatment remains unscheduled, and where the schedule has holes over the next 30, 60, or 90 days. That is where future revenue often shows up first.

Investors should also pay attention to how case acceptance, fee schedules, labor, and reporting are managed. These are not clinical questions. They are business questions.

Investor diligence lens

01

Collections: Is the practice collecting what it produces, or is revenue getting stuck after treatment is completed?

02

Schedule discipline: Are hygiene, recall, and unscheduled treatment being managed before revenue softens?

03

Case acceptance: Are patients getting clear communication, financial guidance, and follow-up after diagnosis?

04

Labor and workflow: Is expensive staff time being used on high-value work, or consumed by tasks that could be centralized, automated, or outsourced?

05

Reporting: Does management see the numbers weekly, or are they waiting for month-end financials to explain what already happened?

None of those questions require an investor to understand dentistry at a clinical level. They reveal whether the operator has visibility, discipline, and a repeatable system for improving each location.

Buying practices creates scale. Improving practices creates value.

The investor takeaway

The most important lesson is simple: dental value creation is operational before it is financial.

The best dental management teams are not merely buying practices and hoping more patients show up. They are improving the business systems that convert clinical care into reliable cash flow.

That means revenue integrity, scheduling discipline, patient reactivation, case acceptance, hygiene retention, labor efficiency, dashboards, accountability, and same-store growth.

Buying practices creates scale.

Improving practices creates value.

Those are the invisible upgrades.

Investors do not need to become dental billing experts. But they should understand the major levers. When evaluating a dental investment, the right question is not just how many practices the operator can buy. It is whether they can make each practice better after they buy it.

The real value-add shows up after closing, when better systems start turning existing patient care into more durable cash flow.

As always, I'm happy to compare notes on this or other private investment models.

This article is for educational purposes only and does not constitute investment advice or an offer to sell securities.

This educational content is designed for sophisticated and accredited investors seeking to understand private-market structures. It is not an offer to buy or sell securities. Always conduct your own due diligence or consult a licensed advisor before investing.